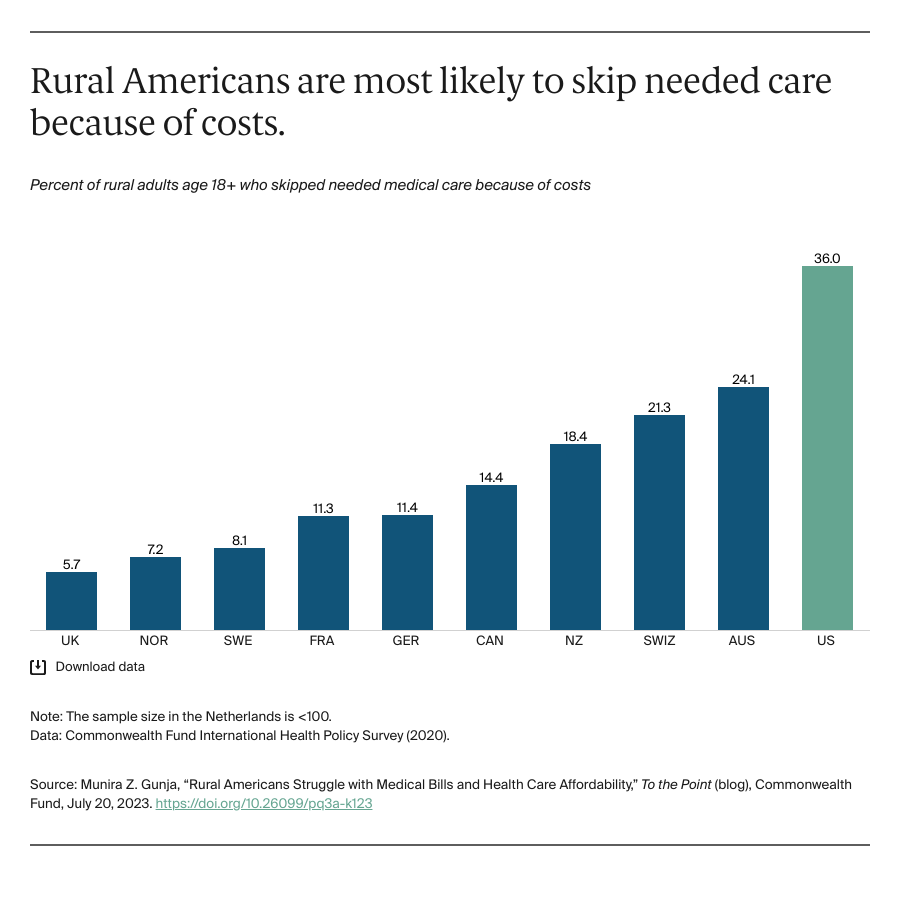

More than one third of Americans living in rural areas skipped medical care they needed due to the costs, according to a new study.

The Commonwealth Fund’s 2020 International Health Policy Survey found that 36 percent of rural Americans did not get the care they needed due to costs, which is more than double the rate for rural residents in six of the other countries the study looked at. Less than 10 percent of rural residents in the United Kingdom, Norway and Sweden reported that they did not get medical care due to costs.

The study looked at 10 other high-income countries besides the United States, including Australia, Canada, France, Germany, the Netherlands, New Zealand, Norway, Sweden, Switzerland and the United Kingdom. Out of these countries, rural residents in the U.S. were most likely to report they struggle to pay their medical bills.

The survey found that nearly 25 percent of rural Americans reported serious problems with being able to pay their medical bills or not being able to pay them at all. In nine of the other countries, less than one in 10 rural residents reported the same thing.

The survey noted that the 10 other countries looked at all had a universal health care system, which the U.S. does not have. The survey also pointed to census data that showed about 12 percent of the American rural population does not have health insurance as a reason why the U.S. fell short of what the other countries reported.

The study also pointed to the disparity in health facilities and pharmacies in rural America compared to other places in the country when talking about the differences between the U.S. and the other high-income countries. It also noted that other countries use Telehealth systems more than the U.S. does, especially in rural America where many do not have access to that technology.

“Rural Americans are more likely to report financial barriers to utilizing health care compared to rural residents in any other high-income country,” the study states. “With affordability problems preventing Americans from seeing their doctor, it is no surprise that rural Americans also are more likely to have higher rates of chronic conditions and some of the highest rates of mental health conditions.”